[ad_1]

Vitality Switch (ET 2.32%) gives buyers the most effective of each worlds. The grasp restricted partnership (MLP) has an enormous yield (presently round 8.5%). Due to that, it might present buyers with a variety of revenue. The primary motive it has such a excessive yield is it trades at a bottom-of-the-barrel valuation. That provides it important appreciation potential.

These options make it an excellent alternative for these with $1,000 or much less to speculate. It has the potential to provide a high-octane total return.

A gorgeous and rising revenue stream

Vitality Switch generates a variety of regular money circulation as secure, fee-based constructions provide about 90% of its earnings. The midstream firm produced about $7.6 billion of distributable money circulation final yr. It distributed about $4 billion to buyers, enabling it to retain $3.6 billion of its money circulation. That provides this MLP an enormous cushion, serving to put its big-time payout on a particularly agency basis.

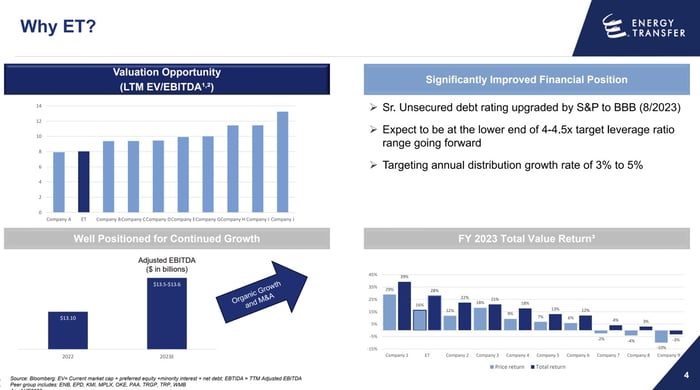

The MLP used its retained money to fund enlargement initiatives (about $1.6 billion final yr) and strengthen its stability sheet. That gave it the flexibleness to make two acquisitions final yr. Even after finishing these offers, the corporate expects its leverage ratio to be within the decrease half of its 4.0 to 4.5 instances goal vary this yr. That function places its high-yielding distribution on a good firmer basis.

Vitality Switch’s secure money circulation, low payout ratio, and robust stability sheet imply buyers can financial institution on its 8.5% yielding distribution. The MLP would flip a $1,000 funding into about $85 of annual passive revenue at that charge. That is a pleasant base return, particularly when the dividend yield of the S&P 500 is lower than 1.5% (which means an investor would generate lower than $15 of annual revenue in the event that they invested the identical quantity in an S&P 500 index fund).

The corporate’s present yield is simply the place to begin. Vitality Switch expects to extend its distribution by about 3% to five% yearly by elevating its cost barely every quarter. That can provide buyers with a steadily rising revenue stream.

Filth low-cost with upside catalysts

The primary motive Vitality Switch has such a excessive yield is its dirt-cheap valuation:

Picture supply: Vitality Switch.

Because the chart within the higher left-hand facet of that slide reveals, it has one of many least expensive valuations in its peer group. That drives the view that Vitality Switch has significant upside. The common 12-month value goal of analysts who comply with the corporate is $18.13 per unit (greater than 20% above the present value), whereas the high is $22 per unit (roughly 50% above the present value).

Vitality Switch has numerous methods to slim that valuation hole. One potential choice is to make use of a few of its rising extra free money circulation to repurchase a few of its items. The MLP’s long-term capital-allocation technique would see it pay about 53% of its money in distributions every year (roughly $4 billion), reinvest 27% to 40% on enlargement initiatives ($2 billion to $3 billion), and use the remaining 7% to twenty% on debt discount and unit repurchases ($500 million to $1.5 billion). With its capital spending anticipated to be $2.4 billion to $2.6 billion this yr and its leverage ratio trending towards the decrease half of its goal vary, it ought to have the flexibleness to launch a unit-repurchase program in 2024.

One other potential upside catalyst is lastly approving its long-delayed Lake Charles LNG mission. It is working to safe closing approvals and the companions needed to move forward with the project.

Lastly, the corporate is able to continue consolidating the midstream sector. It made two acquisitions final yr, which, together with enlargement initiatives, ought to gas 7% earnings development in 2024. Its most up-to-date acquisition (a $7.1 billion merger with Crestwood) is progressing higher than anticipated. Vitality Switch anticipates capturing $80 million of merger synergies, double its preliminary expectation. It additionally sees the potential for future industrial synergies. One other needle-moving deal like that would assist additional increase its earnings and, ultimately, its valuation.

Excessive-octane whole return potential

Vitality Switch’s high-yielding distribution can provide buyers with a pretty and rising revenue stream. In the meantime, the MLP has numerous upside potential on account of its low valuation. It has a number of catalysts on the horizon that would assist slim the hole. These components might give the MLP the gas to provide sturdy whole returns. That makes it an excellent place to speculate $1,000 proper now to earn a robust and steadily rising revenue stream with significant price-appreciation potential.

Matt DiLallo has positions in Vitality Switch. The Motley Idiot has no place in any of the shares talked about. The Motley Idiot has a disclosure policy.